Experts have roundly criticized BC Premier Christy Clark’s recent home ownership grant policy. A key part of the negative reaction has been based on fears that interest free grants will increase housing prices and drive a further wedge between incomes and housing costs, a divide already plaguing the Vancouver and lower mainland markets.

These worries about the divide between housing prices and incomes are well founded.

Trends in residential property prices and housing affordability between 2005 and 2016 paint a grim picture in both Vancouver and the city of Toronto. This article looks at those trends, analyzing the mortgage cost of homes in these two cities and in comparison to Canada more broadly.

More specifically, it looks at the number of weeks of labour time it would take workers making the average weekly wage to make a mortgage purchase in each city. The data are startling.

Methodology:

The nominal dollar cost of a house or a condo today is much higher than it was 10 or 20 years ago. Indeed, it is even higher than what it was just a couple of years ago. There exists a number of indices that look at the price of housing by deflating the nominal dollar price of a house by the consumer price index (CPI) to get an idea of how fast housing prices are rising relative to the general rise in prices of consumer goods.

This article does something different. It calculates how many weeks of labour time, paid at average provincial weekly rates, it takes to purchase an average residential property. In order to do so, it makes some key assumptions.

The calculations in this article concern changes in the mortgage costs of residential property purchases. Here, I assume that the entire price of the properties (inclusive of mortgage fees and financing costs) were paid through a mortgage financed with 5-year mortgage loans amortized over 15 years. In other words, it assumes no initial down payment. By looking at the weeks of labour time, the analysis assumes that all of a person’s income is going towards financing their mortgage. Of course, we know people have many other fixed costs and financial responsibilities. But this measure gives us an informative picture of the glaring gap between incomes and housing prices.

Of course, since we don’t know what interest rates and wage rates will be after 2016, the numbers for the years after 2011 are estimates based on an extrapolation of recent data for these two variables. The calculation also assume, after 2011, a return towards trend values in the case of interest rates). Finally, the data is based on yearly averages. So for the year 2016, with the series ending in June, the average was calculated for the first six months. As a result, the calculations most likely underestimate what will be the true 2016 values.

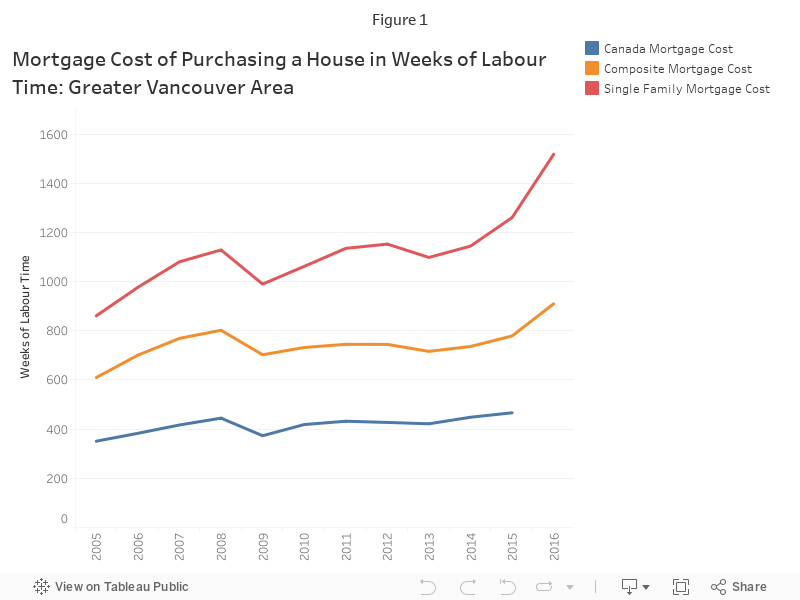

Vancouver

Unless they inherit from their parents, most Vancouverites are unable to purchase residential property outright with a cash payment. It is helpful then to look at how much it costs in terms of weeks of labour time to purchase the average residential property when individuals finance their purchase through a mortgage.

The increases in the mortgage prices of dwellings in Vancouver look disturbingly like a bubble. The data show it took 610 weeks of labour time to buy the average Vancouver dwelling through a mortgage in 2005, or nearly 12 years. It is estimated that it will take 910 weeks, or 17.5 years, to do so in 2016.

Growing unaffordability is even worse for single family houses which required 861 weeks, or 16.5 years of labour time in 2005 to cover the mortgage cost. In 2016, it is estimated to be no less than 1518 weeks — that’s over 29 years. Figure 2 also illustrates how the Vancouver housing market differs in the more pronounced severity of its affordability challenge as compared to the country as a whole.

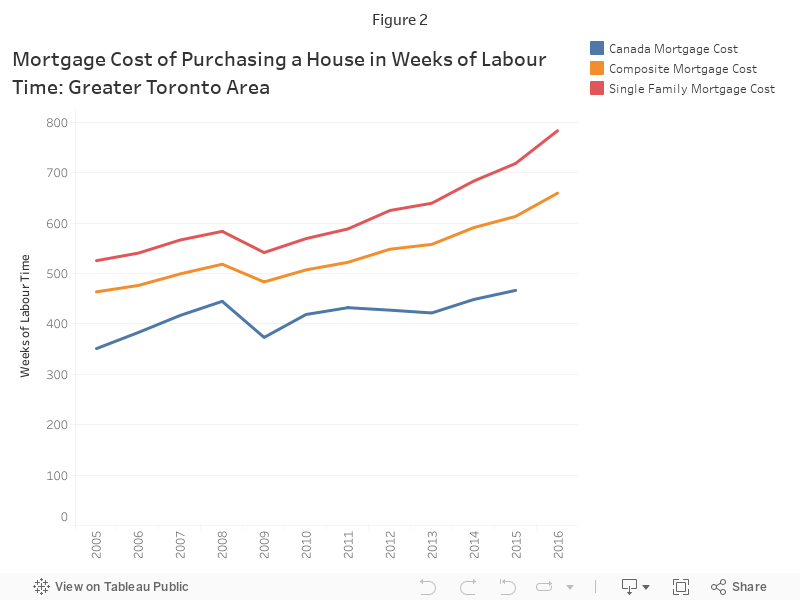

Toronto

The situation of the Greater Toronto Area (henceforth Toronto) has shown a similar trend to that of Greater Vancouver. Figures 2 applies the same methodology as the preceding analysis of Vancouver however using the average weekly wage in Ontario.

When purchased through a mortgage, it took 513 weeks of labour time or nearly 10 years in 2005 to buy the average Toronto dwelling. It is estimated that it will take 652 weeks of labour time, or 12.5 years, to do the same in 2016. Single family houses, once more, show a more marked divergence. Mortgage purchases required 526 weeks of labour time in 2005 (almost 10 years) and no less than 15 years, or 783 weeks, in 2016.

While conditions for first-time homeowners in Toronto area are clearly worsening, and are pronounced compared to those in the rest of Canada, they pale compared to the conditions faced by those living in the Greater Vancouver area. It takes roughly twice as many weeks of labour time measured in the appropriate provincial mean weekly wage to buy a dwelling through a mortgage in Vancouver than in does in Toronto.

Affordable housing increasingly illusory

These data point to stark and growing disparity between incomes and housing prices since 2005, far outstretching a related but less pronounced trend in the rest of the country. If the analysis had looked at median income, the results would likely be even more stark.

Current and recent home buyers in Toronto and Vancouver are devoting many more weeks of labour time to the financing of their home than their predecessors and the dream of home ownership is becoming increasingly remote for all but the wealthiest and highest income earners.

The effects of growing housing affordability are not isolated to Toronto and Vancouver. The Canada Housing and Mortgage Corporation, Canada’s housing agency, recently warned that prices are soaring in British Columbia and Ontario as the real estate boom in Vancouver and Toronto spread deeper into surrounding communities.

Housing affordability is a complex public policy challenge and addressing it, and the inequality and cost of living challenges it betrays, will require a myriad of public policy measures. The case for further government action is clear not only on housing but on wage growth as well.

Marc Lavoie is Professor in the Department of Economics at the University of Ottawa and Broadbent Institute policy fellow. This research was financed by a grant that Mario Seccareccia and Marc obtained from the Institute for New Economic Thinking (INET). Thank you to economist Sheila Matthen for graphs.

Image:Karen Neoh CC BY 2.0