Table of Contents

About the Author

Alex Purdye is a research analyst and a master’s student at Carleton University’s Institute of Political Economy. His research focuses include monetary theory, currency internationalization, classical political economy, and the history of economic thought.

Executive Summary

This report examines the Canadian grocery industry to better understand what is driving retail profit growth, and as a result, higher supermarket food prices. Currently, there are two dominant narratives about grocery profit growth. The first is that demand growth in the pandemic and post-pandemic period has driven profit increases. This argument is highly unlikely given that the real sale volume of food items has declined since the 2020 peak.

The second argues for “greedflation”—the idea that inflation is being driven by corporations using inflation as an excuse to increase prices and squeeze consumers for higher profits. Greedflation is a loose analytical term, but this essential idea that inflation and profits are increasing at the same time is correct. To narrow the definition and look at the underlying movements in the market, this report will look at the process of greedflation through the lens of “seller’s inflation”—a framework for analyzing competition that has become widely noted in the post-pandemic period.

There are three key findings from this report:

- Grocery industry real wages grew substantially from 2018-2020, but since then inflation has negated those gains, regressing wages back to 2018 levels. The decline in real wages has been concurrent with an increase in corporate grocery retailer profits.

- The dynamic between price increases, wage decline, and profit growth are consistent with seller’s inflation, as prices and profits grew alongside these declining wages.

- The grocery industry, even prior to the onset of seller’s inflation, is concentrated. However, a full analysis of competition in this environment can indicate that simply breaking up large firms will not necessarily impact wages or prices without addressing windfall profits and financialization.

In finding that the dynamic of seller’s inflation has occurred, three recommendations can be put forward to aid grocery industry workers in their struggle to increase real wages, alongside retail price stability or decrease for grocery store consumers.

- Windfall profit taxes can be used to reduce incentives for profiteering. This would have the effect of placing a cap on the amount of profit that industry retailers can make, thereby incentivizing either price reductions or wage increases.

- Price controls in systemically significant sectors can function as emergency price stabilizing mechanisms in times of supply crises. They should be incorporated into the federal government’s tool kit to mitigate seller’s inflation.

- Strengthening organized labour helps ensure that when profit windfalls happen in an inflationary environment, that workers get fair wages.

Together, these recommendations serve to strengthen the bargaining position of labour and mitigate sudden price increases and excess profits.

Introduction: Sellers’ Inflation

While orthodox economic theory generally emphasizes the role of labour in causing inflation, particularly pointing to employment expectations and wage growth as sources of price increases, this pattern does not necessarily hold for the grocery industry in Canada from 2020 onwards. Rather, as a 2023 report by the Canadian Centre for Policy Alternatives highlighted, data measuring economic growth from this period, without exports, indicates that the revenue from price increases went to profits, not labour costs.

“Seller’s inflation” is an economic theory of inflation that highlights the relationship between wages, profits, and inflation. It is a dynamic theory drawing on economic thought from the mid-20th century—the so-called golden age of capitalism. Seller’s inflation argues that when costs for firms increase due to a “supply shock,” such as a pandemic lockdown or shipping hold up, price increases can be passed through to consumers either at par value or through an increase in the markup rate.1 This results in an increase in corporate profitability concurrent with a decrease in the real wages of workers. Eventually, this can lead to “conflict inflation” occurring when workers attempt to increase their wages to regain losses made throughout the process. However, in response to demands for increased wages, firms may increase prices further to protect their profit margins to normalize the new high profit level watermark left by the previous supply shock period.

The seller’s inflation approach is broken up into three stages: (1) the “impulse stage” in which the cost shocks occur; (2) the “propagation/amplification stage” where production price increases are either passed through to consumers or increased beyond the pass-through level, and (3) the “conflict stage” wherein labour bargains for wage increases to offset the decline in their real wages.

To assess whether this framework applies to the Canadian grocery retail industry, there are two relevant factors to consider.

First, it must be determined if there are supply shocks affecting costs that occur that have increased prices throughout the supply chain. For the grocery industry, the two most directly relevant factors are energy price shocks and food production price shocks.

Second, the movements of wages, prices, and profits must be determined. For seller’s inflation to hold true, there needs to be a decline in real wages alongside an increase in both prices and profits.

In analyzing these movements, we can determine the first two stages of seller’s inflation and thereby develop a framework for analyzing the motivations behind seller’s inflation as well as regulatory changes and other public policies that can facilitate wage increases and affordability as a response. Given that the present moment in late 2023 indicates a conflict stage with labour acting for fair wages in the grocery sector, of immediate concern is analysis and implications of real wage increases.

Stage 1: Grocery Supply Chain Prices and the “Impulse Stage”

The impulse stage of seller’s inflation is induced by an initial negative price shock, such as a supply chain hold up caused by a COVID-19 pandemic lockdown, that increases the price of industrial inputs, such as the cost of production, which causes firms to respond by increasing their prices on consumers.

In looking at recent price increases compared to the pre-pandemic period, four major price shocks from 2020 onwards can be identified: (i) climate change-related costs, (ii) supply chain bottlenecks, (iii) the Russian Invasion of Ukraine, and (iv) profiteering in the energy sector.

i. Climate Change

Climate change is a highly relevant factor in the production of agricultural commodities. Though agricultural firms have tried to insulate themselves from weather patterns since the “Green Revolution” in agricultural technology throughout the 20th century, the world food system is still beholden to the natural growing environment.2 Over the past several years, climate change-related events have reduced agri-commodity yields. A recent Intragovernmental Panel on Climate Change (IPCC) study indicated a strong relationship between climate change and crop yield reductions. Climate change effects on the global food supply include reductions in arable land, increases in surface ozone, ocean warming depressing the fish supply, and warming reducing soil quality. Additionally, with increases in global temperatures, there are necessary reductions in viable working hours. The danger of working in high temperatures have led to an increase in global agri-worker mortality, and the necessary reduction in working time negatively impacts yields.

So substantial is the problem of climate change that in the past three years, every North American growing season has been severely impacted. In 2020, the Northeastern, Midwestern, and Western United States suffered the worst U.S. droughts of the 21st century, with the Pacific Institute claiming that 70% of the Western U.S. faced severe drought that year. Droughts then affected crop yields in Canada and Mexico in the summer of 2021. Most recently, drought conditions have facilitated massive wildfires sweeping throughout Canada that have negatively impacted growing conditions, razing crops, increasing ozone levels, forcing workers to evacuate, and destroying inputs.

A recent Agriculture and Agri-Food Canada drought assessment indicated that in 2023, drought conditions negatively impacted growing conditions across Western Canada, with Alberta only receiving 40%-60% of its normal precipitation, and Lethbridge specifically receiving below 40% of normal precipitation. These climate change effects have influenced poor yield projections for growing seasons, which is likely to continue to affect food prices in the long-term.

ii. Supply Chain Bottlenecks

International maritime shipping is foundational for the global food supply chain. At all levels of production and retail, shipping, both between and within firms, allows for multinational operations and trade to exist, and interruptions can have major economic consequences. During the 2020 Suez Canal blockage, an estimated value of $9.6 billion USD in trade per day sat idle until the bottleneck was resolved.

The COVID-19 pandemic also caused substantial issues in the management of these essential supply chains. Production and processing centre shutdowns led to backlogs in shipping and production logistics. This occurred both within the food industry itself, and in related industries such as input manufacturing and energy production. Declines in the productivity of shipping drove up costs, as well as during the earlier periods of the pandemic. Though bottlenecks have relaxed in the years since, Canadian shipping continues to be poor, with major ports in Prince Rupert, Halifax, Montreal, and Vancouver all placing below average for time efficiency of vessels in port. Poor supply chain operations persist, though improvements have been made with the relaxing of COVID restrictions.

iii. The Russian Invasion of Ukraine

During the 2022 Russian invasion of Ukraine as part of the ongoing Russo-Ukrainian War, commodity prices increased dramatically. This recent stage of the conflict helped to destabilize two of the most important exporters of agri-commodities in the world. Together, Russia and Ukraine account for 12% of globally traded calories. The ongoing armed conflict places significant pressure on the ability of these countries to engage in trade and production necessary to maintain global food security. While regionally, Canadian food supply is not at risk, the Russo-Ukrainian war does threaten global food affordability, partially influencing inflationary grocery store pressures.

Beyond being a grain producer, Russia is also the world’s largest exporter of finished fertilizer and fertilizer intermediaries. Reductions in the fertilizer supply can cause pressure on growing cycles, raising input costs for food producers. While the Russian agricultural sector, including inputs, is sanction exempt, there are still major disincentives for doing business with Russia. Banking restrictions, fear of political and financial repercussion with future sanctions, and fear of public and internal relations problems have led to reduced Russian exports.

Ukraine is a large exporter of wheat, corn, barley, and sunflower oil. In the three years preceding the war, Ukraine accounted for 10% of global wheat exports and 15% of global corn exports. However, since the start of the war, an estimated $6.6 billion USD in agricultural infrastructure has been destroyed, leading the Ukrainian government to estimate $34.25 billion USD in lost revenue. This is especially problematic since Ukraine is recognized as a low-cost wheat exporter, with lower factor costs allowing them to compete in price sensitive markets and depress global wheat prices.

Earlier during the invasion, the United Nations’ effort to head off food supply problems with the “Black Sea Grain Initiative” appeared initially successful. An agreement between Russia, Ukraine and Turkey which would allow some maritime shipping to stay open through the Black Sea. However, in July 2023, the initiative expired, and the parties have failed to renew it. Without the agreement’s renewal, further disruptions to food and fertilizer exports from Russia and Ukraine could continue to influence global food production costs.

iv. Inflation in the Energy Sector

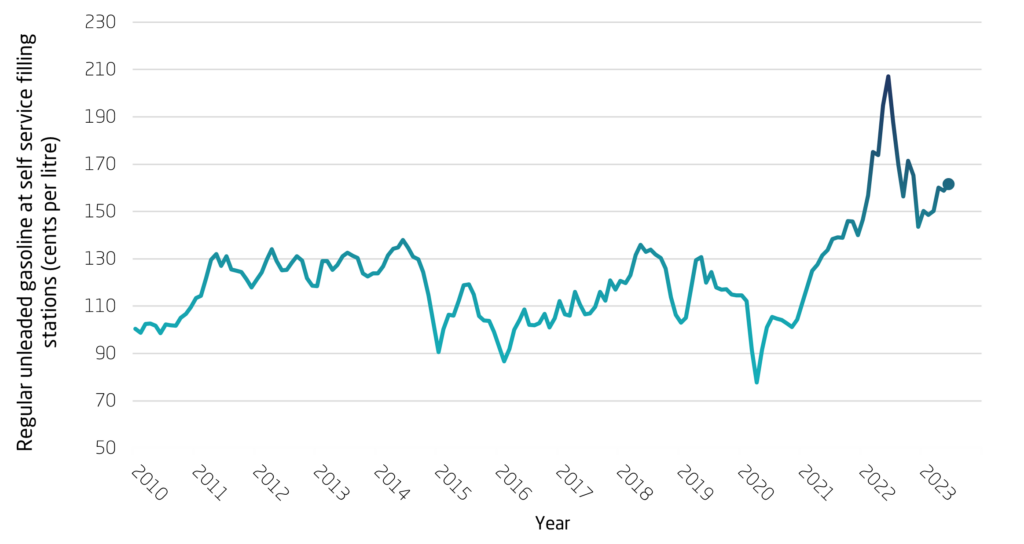

Another influential inflation driver has been the global rise in energy prices throughout the post-2020 period. From a 10-year low in 2020, gas prices steadily increased throughout 2021, with a substantial spike in 2022 with the Russian invasion of Ukraine. This is, in part, to be expected given the importance of both Russia and Ukraine as energy exporters. The war doubled global average household energy expenditure.

However, the rise in energy prices cannot be solely attributed to negative supply shocks. The energy sector is highly concentrated, and the increase in energy prices has also been characterized by an increase in the profits of the energy and oil and mining industry. Recent Canadian analysis carried out in early 2023 demonstrates that most of the pandemic-induced increases in energy prices in Canada fed into profits, rather than increasing labour force wages related to higher productivity. This indicates that prices were likely driven higher by not only increases global prices, but by increases in energy sector profit margins.

The effect is an increase in profits for the industry, alongside a general increase in prices across the economy. Energy is not only important as a direct retail cost, but also for production and supply chain transport. This creates a parallel problem, not unsimilar to the issues faced during the mid-2000s food price surge, wherein increases in crude oil prices were a major contributor to the food crisis that preceded the Great Recession.3

Chart 1 – Monthly average retail prices for gasoline, Canada, 2010-2023

As illustrated by several examples, a variety of global and national supply shocks have influenced higher prices for grocery industry inputs such as food production and supply chains. A series of events beyond the immediate control of grocery retailers have indeed caused their input prices to increase, but the effect of this process relates to the seller’s inflation approach insofar as these costs are passed through to consumers in the form of higher retail prices and met with stagnant real wages for their workforce.

Stages 2 & 3: Wages, Prices, and Profits: “Amplification and Propagation Stage”

Given the existence of negative shocks, it is necessary to look at the empirical data for the movements in wages, prices, and profits that follow these events. For seller’s inflation, data on the grocery retail industry would indicate an increase in prices and profits concurrent with declining wages.

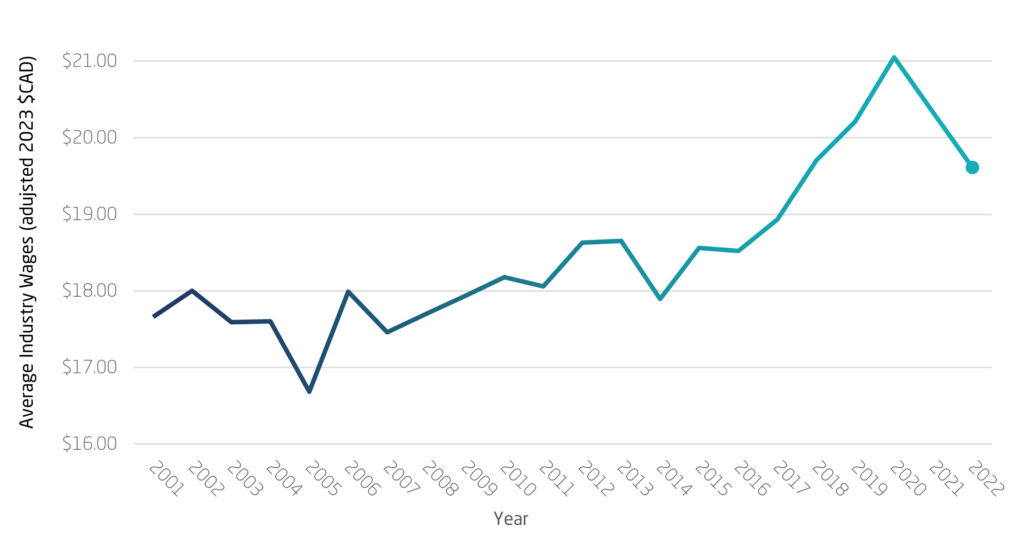

The result of inflation has been a recomposition of grocery industry firm income distribution (the division of income between labour and capital), where there is a decline in the labour share of income alongside an increase in retail prices and profit margins. Examining grocery retail wage data over the past two decades, it is evident that real wage gains made across Canada in the years before the pandemic supply shock have since been negated by price increases. Wage struggle gains, realized in actions such as bargaining and minimum wage hikes, for example the substantial minimum wage hikes in British Columbia under the provincial NDP government’s minimum wage inflation peg strategy, were reversed by the inflation surge of 2022-2023.

Examining wages in 2023 Canadian dollars, nation-wide average industry wages rose from $19.70/hour to $21.50/hour in 2020. This represented a break from the preceding decade and a half, doubling the real wage gains won in that period. In part, the 2020 figure was established through organized labour’s successful push for the $2.00/hour “hero pay” increases, which temporarily increased hourly wages for essential workers until grocery retailers rolled the increases back, sparking a national wage-fixing scandal and legislative changes to target wage-fixing. However, in the following two years, wages have regressed to $19.61/hour, eliminating the hard-fought wages gains, as demonstrated by the wage date in Chart 2.

Chart 2 – Real Wages in the Grocery Sector Across Canada, 2001-2022

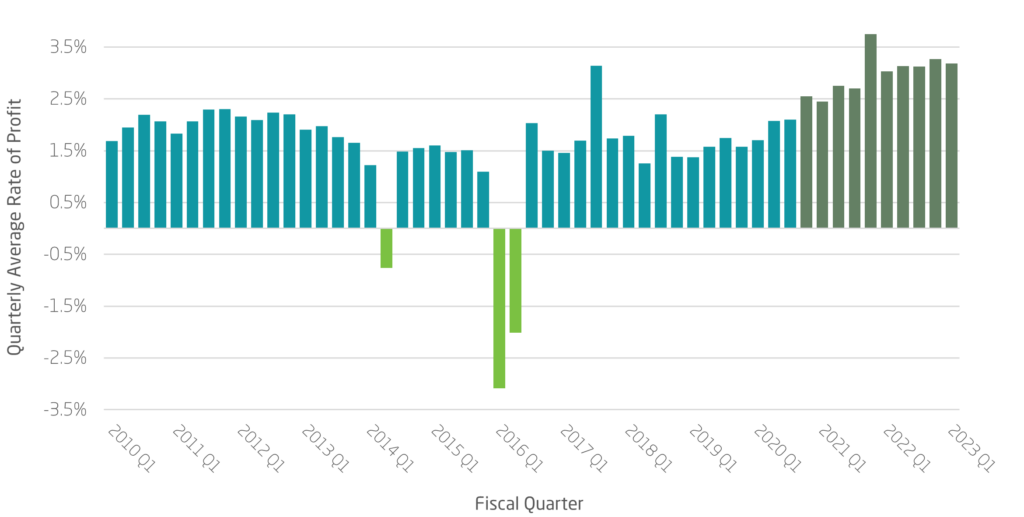

Simultaneously, the net profit margins for food and beverage stores (defined as net income/total revenue) have increased from 1.79% in Q1 2018 to 3.27% in Q4 2022 an 82.68% increase in net profit margins. While consumer focused reports such as the report on grocery prices for the standing committee on agriculture and agri-food, have been met with the claim that this increase in profitability may be a result of an increase in higher margin non-food items, this neglects the increase in profitability stemming from a decline in real wages.

Chart 3 illustrates the relationship between industry wages and net profit margins. Chart 4 highlights the long-term trend in subsector net profit margins, with recent years marking historically high consistent net profit margins.

Chart 3 – Food and Beverage Stores: Annual Real Wages (2023 $CAD) vs. Annual Rate of Firm Profits Across Canada, 2018-2022

Chart 4 – Food and Beverage Stores Quarterly Average Rate of Profit Across Canada, 2010-2023

Stage 4: “Conflict Stage” Analysis: Wage-Share/Profit-Share

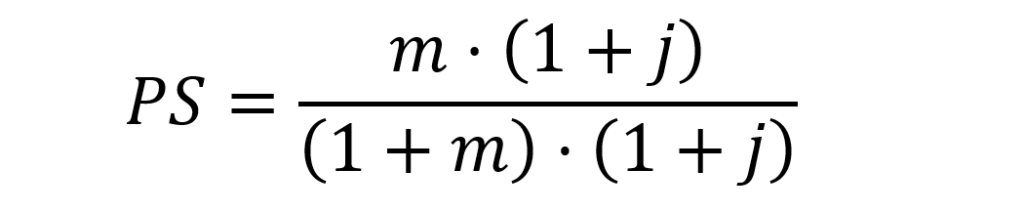

Using a wage-share approach, this rapid growth in profits and decline in real wages can be analyzed. With a simplified profit-share equation, it is evident that inflation has the effect of depressing real wages with stable markups and increased material costs.

If ps = the profit share, m = the markup rate, and j = unit material costs/unit labour costs, then a simplified post-Keynesian profit equation demonstrates this dynamic.

Holding the markup rate constant, a relative increase in unit material costs over unit labour costs will always generate an increase in unit profit margins. As such, changes in net profit margins from 2021-2022 were primarily generated at the expense of real wages. According to economist Jim Stanford in early 2023, “data confirms that aggregate profits have doubled since pre-pandemic norms.”

Grocery profits are then as much a question of labour as they are of consumers at the checkout line. Some commentators argue that a 10% increase in grocery clerk wages would require layoffs to prevent an increase in retail prices. However, this is argued from the perspective that the grocery retail business model of high-volume, low-margin sales is antagonistic to wage increases. Wage profit trends in the past few years demonstrate that labour is being squeezed for real wages to increase profitability. Perspectives pushing for job cuts amid high prices come from traditional economic theories that fundamentally misunderstand the micro dynamics of businesses. An increase in wages does not necessarily have to be met with a parallel increase in retail prices—as evidenced by the period between 2018 and 2020 wherein prices grew at pace with inflation while real wages rose—it can occur alongside a decline in profits or a long-run increase in the efficiency of the labour process.

The arguments used to dismiss labour’s diminishing income by fear mongering higher prices have been used since the development of the modern industrial labour movement during the Industrial Revolution. Highlighting rising grocery prices can be used as a deterrent to public support for workers’ wage gains—a reasonable concern given the rate at which grocery prices have increased financial strain for working-class Canadians, with a marked increase in food bank use and food insecurity. The often-discussed “wage-price spiral,” in which a high-cost living causes workers to demand higher wages leading to higher prices, is typically used in narratives arguing against raising wages to relieve inflationary affordability pressures.

Inflation is not a natural and predetermined phenomenon, existing in an abstract vacuum and forced into life when workers try to better their conditions. It is a pricing strategy set by firms, and one designed to increase profitability at the expense of labour and consumers. Increased prices reflect this desire to maximize profitability by reducing labour costs. This is especially true following periods of strong organized labour in which profits are limited in favour of wages. Firms can independently reduce their net-profit margins to allow for greater wage increases, accommodating a higher labour share of income, and simultaneously, regulatory changes can modify the competitive conditions that facilitate firms’ efforts to squeeze workers and consumers, aiding organized labour in their efforts to increase worker wages.

This is especially prudent in the Canadian grocery industry. The current net profit margins for food and beverage stores exceeds historic levels and global standards. Grocery retailer net profit margins for large firms tend to sit between 1% to 3%.4 The present increase in large Canadian grocer’s profits exceeds the upper boundary of the industry standard. However, as demonstrated by the gains made by labour prior to the COVID-19 pandemic, this favourable shift for profit as a share of firm income is not inevitable. There is a trade-off between labour, consumers, and corporate profits. Increases in wages and lower prices can occur if they happen alongside a decline in net profit margins.

Raising real wages is an especially pressing concern for the industry right now. The cost-of-living crisis that has long plagued Canadian workers has been exacerbated in the post-2020 period. In response to inflation and real wage declines, two-in-five Canadian households are drawing on savings or taking lines of credit to sustain themselves. This is especially true for low-wage workers in major urban centres. In Toronto, housing cost burdens with more than a 50% income ratio as associated with decreased material well-being.5

This is a prudent concern with real wage declines occurring alongside real increases in rental and housing prices, with a 1.8% increase in Canadian month over month rents in July 2023 alone. Paired with other inelastic living requirements, such as the 19.6% increase in food costs between 2020 and 2023, Canadian household economic stress is a major problem. The situation has become so dire that 25% of Canadians are unable to meet an unexpected expense of $500.

“Conflict Stage” Causes: Competition and Financialization

While the seller’s inflation process is clear in terms of preconditions (impulse) and outcomes (propagation), there exists a theoretical problem at the heart of these price increases, how were firms able to raise their prices?

Explanations around this generally take recourse to competition problems, as indicated by the Competition Bureau’s market study to examine the level of competition. However, classical economic theories regarding competition are insufficient in explaining the current inflationary episode. An understanding of (i) competition, (ii) financialization, and (iii) their implications on labour can help to illustrate the current conflict stage of seller’s inflation more fully.

i. Competing Ideas on Competition

Understanding how competition works in the grocery sector is important in determining whether change in the number of industry players would result in changes in competitive dynamics. In Canada, the House of Commons Agriculture Committee’s 2023 report on grocery affordability recommended that strengthening the Competition Bureau would ensure competition in the grocery sector. However, even a strongly competitive environment may not necessarily lead to socially desirable outcomes, such as lower prices and higher wages.

In orthodox economic thought, it is assumed that competition is derived from the quantity of firms in a given market. In this view, concentrated industries are a deviation from a state of “perfect competition” transforming firms from price-takers, reacting to changes in supply and demand, into price-setters as their market power increases. This allows firms to set prices at above competitive levels, and thereby generate excess profits until demand changes.

This is substantially different from more recent theories on competition, which posit that strategic choices are made in the pursuit of profits.6 In this view, all firms effectively set prices intending to generate different effects both on their short-run profitability and the long-run market structure. This difference can be summed up by labour economist Howard Botwinick:

When business executives speak of a highly competitive market, they often mean one in which each firm is keenly aware of its rivalry with a few others and in which advertising, styling, packaging, and other such commercial weapons are used to attract business away from them. In contrast, the basic feature of the economist’s definition of perfect competition is its impersonality. Because there are so many firms in the industries, no firm views another as a competitor.7

Distinct from this “quantity theory of competition,” the older classical theory of competition has found a resurgence in explaining the present grocery industry inflation. The classical theory of competition focuses not on the quantity of uniform firms within a market, but rather, recognizes that firms within an industry are diverse in their cost structure (i.e., some firms produce at lower costs than others) while also acknowledging that firms do not just compete within their industry, but that there is also competition between industries.8

On cost structures, different corporations within the same industries produce the same goods and services at different costs. This is a fact widely acknowledged in business literature, in which different strategies around pricing develop in response to the different production costs of firms.

The general trend that emerges is that lower cost firms operate at a higher profit margin, as they can either set prices below what other firms are able to sustain or receive a higher profit margin at higher prices. However, cost structures are not static, but rather, are dynamic. They can change over time in response to different conditions and strategies, and, to remain competitive within an industry, firms must continually invest in reducing their costs.

ii. Financialization of Competition

This form of competition can lead to a differentiation of profit margins within an industry, it also creates a process of inter-industry profit-rate equalization. It does so through the relationship between production and finance. This is because the source of competition is not the quantity of firms, but rather the fluidity of finance.9

As the goal of competition is ultimately about seeking profits through short-run decisions, financial capital recognizes which industries have an above-average rate of return. The ability to sink investment into these highly profitable industries allows for investors, depending on the structure of the firms themselves, to generate above average returns. Because of this, the financial services industry is the most competitive of all industries. There is very little friction or time-delay when trading in capital markets (such as stock trading) or investing in firms through direct lending. This lets the financial sector rapidly direct the flow of investment into industries, suppressing or accelerating profitability by withholding or deploying investment. In effect, profit margins within industries are differentiated by cost structures while profit rates between industries are equalized by financial competition.

Because of this, competition is also about outcompeting other industries for a higher return on investment for the financial sector—an increased rate of profit defined as the rate of return on capital. There are also incentives for corporate executives to maximize profits of their companies, who can benefit from short-term increases in stock prices that can further amplify the effects of financialization.

In 1998, a study of the Brazilian market, a country with multiple oligopoly industries, it was demonstrated that concentrated industries did not tend to have higher rates of profit. Rather, it showed that all industries tended to regulate around a general rate of profit across the economy as a whole (though, important to note, never achieving a stable equilibrium rate of profit).10 Recent empirical work has also demonstrated this trend in the U.S. economy most definitively, as well as for the OECD countries at the sector level.11 While these empirical studies are not for the Canadian market specifically, what they reflect is the general structure of how financialized competition operates, particularly as it relates to the process of profit-rate equalization.

iii. The Implications of Financialization on Labour

Beyond the equalization effect of competition supporting price increases and stability, there is also a negative effect on labour. To be attractive for inter-industry investment and maintain competitiveness within industries, firms need to adopt low-cost production strategies that generate higher rates of profit. To do so, cost structures need to reduce the relative price of labour. This can be done in two ways: reducing real wages or increasing labour productivity.

First, an actual decline in hourly compensation can occur through an increase in working hours or a decrease in real wages. However, in advanced market economies, regulations won by organized labour generally prevent the ability to extend working hours without an increase in compensation, often at above average hourly rates, through overtime pay.

In lieu of increasing working hours, this leaves reductions in real wages as the primary approach for firms to reduce labour costs. These reductions do not often occur to nominal wages employers do not directly cut wages from $15/hour to $14/hour in their effort to take profit out of their payroll. Rather, firms manage to obscure their cuts by increasing wages below the rate of inflation, creating a real wage reducing effect without the same level of backlash from workers that would come from a nominal wage cut. This dynamic has occurred through the grocery industry’s approach to seller’s inflation.

Second, an increase in labour productivity to generate higher profits can occur through labour process innovations, introducing new methods of production. Generally, innovation can be delivered through either change to organizational efficiency or through the introduction of new technologies. With the development of new technologies, such as automated checkout counters, firms can reduce costs if the capital costs required to install new technologies are lower than the costs to reduce labour input. This can have a deleterious effect on workers’ income as it is displaced by technology and innovation without additional investment in their own productivity through wage increases. Technological innovation has become a driver behind the dynamism of markets, pushing corporate leadership into a perpetual pursuit for innovations in the labour process to reduce costs and allow for operations to scale.

In the Canadian grocery industry, labour process innovations have been a substantial part of the post-2016 market. After the collapse in profitability in 2016 (as illustrated in Chart 4), the industry increased its focus on cost reductions, and brought grocery stores up to cross-industry retail standards.

Two major developments since this period are represented by Loblaw Companies’ strategy of digitalization and Walmart Canada’s self-checkout modernization.

Loblaw Companies, the firm with the largest market share in the industry, has spent the past half-decade substantially investing in technological growth. This has primarily taken the form of digitalization and the expansion of self-checkout, with their public statement in 2023 explaining:

Over the past five years, Loblaw’s capital investments have evolved with the grocery landscape, driven by digital innovation and technology. This year, it will increase its investment level focusing on its core retail experience, expanding its presence in communities, modernizing its supply chain, and making food and healthcare more accessible.

Similarly, Walmart Canada has massively invested in self-checkout modernization, with a $3.5 billion investment in 2020 for the modernization and adoption of smart technology in more than a third of its stores.

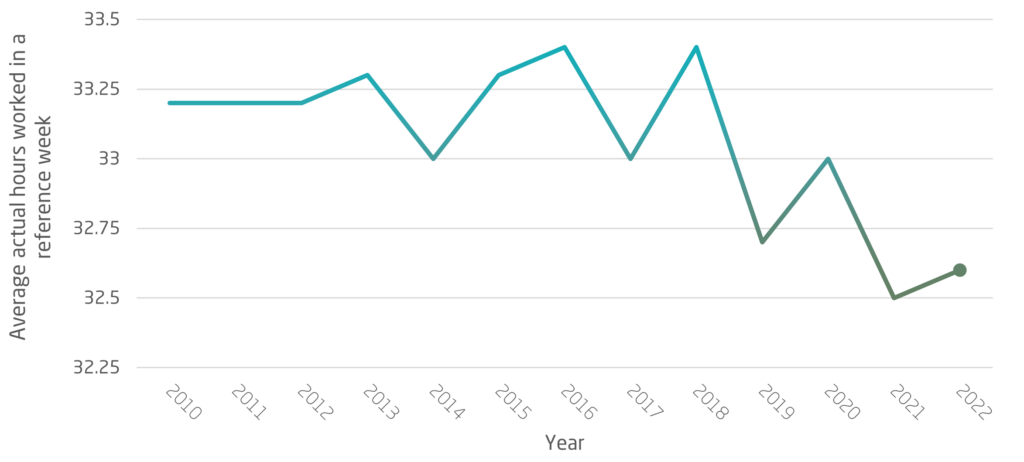

These expansions, focused on cost reduction, can help to explain Competition Bureau Canada’s identified pre-pandemic margin increases. While superficially these investments in innovations can seem like a good thing as increasing profitability can be concurrent with real wage growth and stable sale prices, it can still have a detrimental impact on labour’s power. Because industry unions are strong, firms have difficulty in just laying off workers during periods of stable economic growth. Instead, even during these stable economic periods, there can be reductions in working hours, therefore reducing workers’ real take-home pay (see Chart 5 for reductions in retail weekly hours over time).12 In the long-run, further expansion in self-checkout technology may eliminate a substantial portion of industry jobs, with that money flowing back into profitability instead of labour.

Understanding the centrality of innovation to market economies, and the movements that developed in the grocery industry, it is essential to figure out why these innovations were spurred over the past few years.

Chart 5 – Average actual hours worked in a reference week, main job, wholesale and retail trade, Canada 2010-2022

Canadian Grocery Industry Financialization

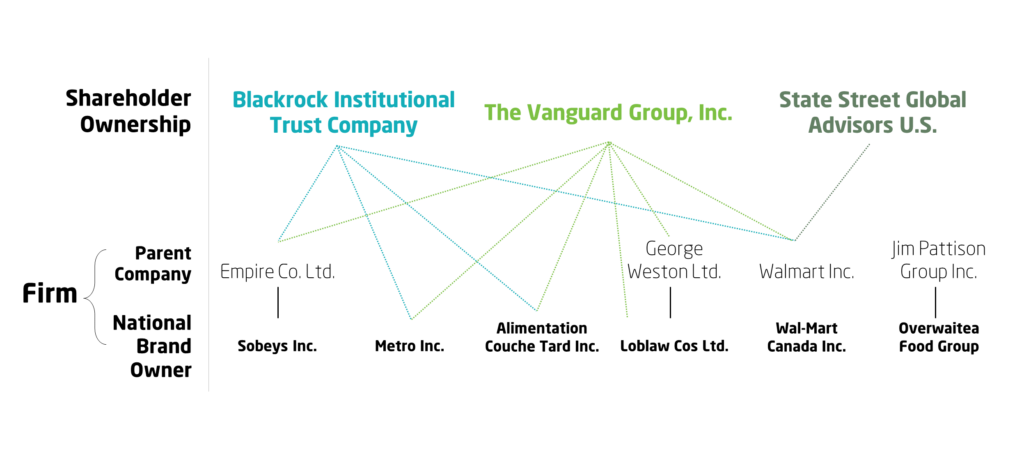

Understanding the recent years of the Canadian grocery industry as dynamic and innovative, the question needs to be raised as to why this process has been occurring following relative stagnation pre-2016 when the grocery industry fell below cross industry retail standards. This is because the grocery industry does not just exist as a site of profit generation through sales, but also as a site of investment for national and international financial service firms.

Figure 1 illustrates the financial linkages between the so-called “Big Three” asset managers and grocery retailers. Table 1 illustrates the institutional investors that are major voting shareholders for Loblaw Companies Ltd.

Figure 1 – Shareholder Ownership of National Grocery Store Companies in Canada

Table 1 – As of September 5th, 2023: Top 10 Shareholder Equity Positions for Loblaw Companies Limited (Stock A Voting Shares)

| George Weston Limited | 14,722 M $ |

| Fidelity Investments Canada ULC | 650 M $ |

| The Vanguard Group, Inc. | 446 M $ |

| RBC Global Asset Management, Inc. | 366 M $ |

| TD Asset Management, Inc. | 327 M $ |

| Mackenzie Financial Corp. | 297 M $ |

| AllianceBernstein LP | 209 M $ |

| Norges Bank Investment Management | 153 M $ |

| Fidelity Management & Research Co. LLC | 138 M $ |

| 1832 Asset Management LP | 138 M $ |

Canadian grocery retailers are strongly integrated into financial markets through capital markets. This sometimes-overlooked characteristic of the current market concentration is relevant as these firms are marginally constrained in their business autonomy. Institutional investment facilitates the need to meet key financial targets, particularly those that maximizes the return on investment for investors. The need to meet these targets intensifies the pre-existing competitive pressures placed on firms.13

After the grocery retail 2016 profit collapse, the finance sector proceeded into a defensive position, seeking ways of scaling and innovating grocery retail that would restore profitability in competition between and within industries. This was a long time coming, according to a 2018 McKinsey & Company report, as the grocery retail industry lagged behind other retailers, making themselves vulnerable to disruptions brought about by e-commerce and becoming undesirable as a site of profitable investment. Fears of financial withdrawal compelled Canadian grocery retailers to increase investments in labour process innovations, which have had detrimental impacts on labour.

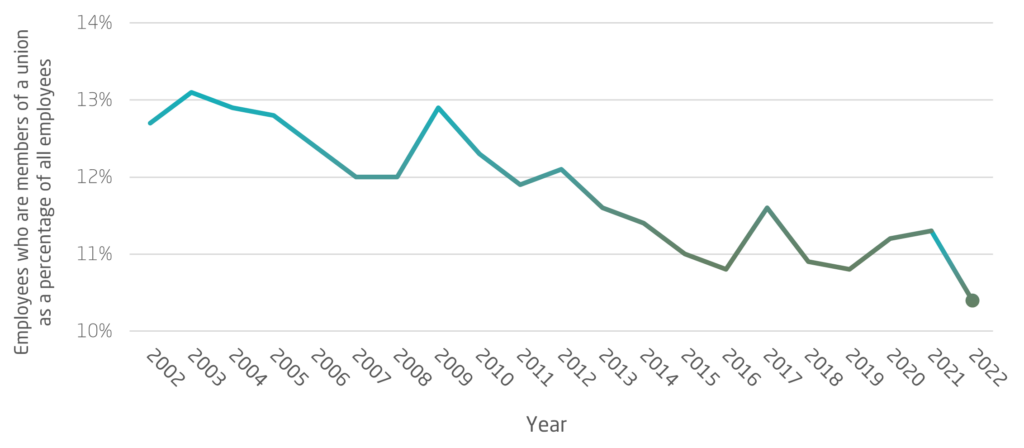

It is largely thanks to the strength of organized labour protecting employment that volatility and job precarity was not made worse, leading to working hour reductions rather than wage cuts and employment loss. It is worth noting that labour unions have long recognized the role of financialization in making their fight for wages and protection harder in the face of declining union density rates.

Chart 6 – Unionization Rate for Wholesale and Retail Trade, Canada, 2002-202214

In reaction, the global labour movement has engaged in “pension fund activism” whereby the substantial amounts of financial assets owned by union pensions are used to attempt to mitigate the negative impacts of financialization.15 However, there has been limited success in this approach as the financial sector has ultimately focused on maximizing returns. The equalization effect of this approach has been driven by the financial sector’s search for profits, and actors are compelled to work within its profit motive.

Market Concentration and Competition

What this current model of competition indicates is that, regardless of the level of concentration in a market, cost-pass-throughs prioritizing reductions in labour costs regulate around higher rates of profit, incentivized by the need for private investment. New investment allows firms to scale their operations and pursue research and development to make the labour process more efficient. The result is that cost-pass-throughs enabled by supply shocks become normalized (though with some differentiation) across industries so that firms can retain their attractiveness as sites of financial investment.

While the Canadian grocery industry is certainly concentrated, with a CR4 “concentration ratio” (a standard measurement of market concentration that demonstrates the market share of the largest four firms) of 68%, concentration among few players does not necessarily mean that the industry is anti-competitive. Where concentration is relevant is only insofar as it can facilitate price collusion, such as in the Canadian grocery industry’s bread price-fixing scandal. Rather, depressing wages and the increase in price that we have seen are the consequence of financialized competition.

This is a relevant perspective when it comes to prescriptive policy recommendations. The often touted need to break up the grocery giants, while a good thing because it will disincentivize price collusion, is insufficient to address the trends of increasing prices and declining real wages. Competition as it stands in the grocery retail industry aims at increasing or retaining profitability for both financial and non-financial firms, and therefore dealing with these trends requires market interventions that directly target profits. While improving competition is complementary to regulate the industry, a number of other policies and strategies must be put forward to attenuate profiteering and financialization among Canada’s grocery retailers.

Recommendations

Three policy recommendations can be put forward to address seller’s inflation and the other affiliated problems stemming from financialized competition. At the propagation stage, where policy intervention can have a major impact, three interrelated solutions could have a wage increasing effect, while moderating profits: (i) a windfall profit tax; (ii) price controls; and (iii) strengthening the bargaining power of organized labour.

A key principle of social democracy aims to reduce people’s reliance on the free market to meet their needs.16 Together, these three interventions constitute a turn away from a market-determined food system in Canada.

i. Windfall Taxes

Windfall taxes are imposed on companies or whole industries that experience sudden and unexpected increases in profits by factors outside of changes within the industry, such as in the case of the grocery industry’s recent seller’s inflation. Windfall taxes on the fossil fuel extraction industry have even been recommended by the International Monetary Fund to aid governments facing pandemic-induced fiscal pressures, contain inflation and induce the transition to renewable energy. As illustrated in Chart 4, prior to 2020 profits in the food industry very rarely exceeded 2.5%.

Windfall taxes on the grocery industry can create a cost incentive for firms to reduce their gross margins, as recommended by the House of Commons Agriculture Committee’s 2023 report on grocery affordability. Their introduction on corporate grocery retailers could disincentivize excess hikes in their profit margins on food items. Beyond the grocery industry, when applied broadly across the economy, this can place a limit on profitability writ large and thereby alleviate inter-industry competition for profits induced by the financial sector. If financiers seek investments that project higher returns, thereby equalizing profits across industries, placing limits on profitability more broadly places limits on the volatility of inter-industry financial flows.

Broad windfall taxes are thereby a relatively straightforward policy tool, negating the power of the financial sector while inducing companies to make productive use out of their windfall profits by lowering prices or increasing wages without high levels of bureaucratic oversight or technical involvement. In the long run, it should change firms’ cost structures and pricing strategies to prioritize market share over profitability. This is invaluable given that firms, in competitive market conditions, tend to not engage in price wars given the potential negative impacts on profits. This creates price stability; however, it also prevents prices from going down or the cost structure changing to accommodate higher wages.

There are, however, limits to this approach. Primarily, it may not have a positive impact on wages. wages are not solely at the whims of corporate strategy. Rather, wages are won by workers in organized struggle, as evidenced by the existence of union wage premiums. The outcome of changing cost-structures under a windfall tax can then be understood as a consequence of the strength of organized labour, as increases in unit labour costs can also be a source of competitiveness in a modified competitive environment.

ii. Price Controls

For intervention at the impulse stage of seller’s inflation, changes to navigating inflationary management are essential. Current approaches may focus on increasing unemployment, reducing wages, and making the labour market more competitive for workers. This approach has a detrimental impact on workers’ livelihoods while, in situations such as cost-shocks, fail to address the underlying cause of inflation. Alternatively, price controls can be considered an emergency strategy to tackle extreme fluctuations during the early stages of negative supply shocks. Weber et al.’s 2022 input-output study has demonstrated that cost shocks move through the economy starting in important input-generating sectors, particularly the energy industry.

This indicates that in the short-run, targeted price controls in systemically significant sectors, such as the energy sector, that have substantial impacts on downstream industries, like grocery retailers, can mitigate cost-shocks and inflation growth. However, there are some important considerations in the implementation of this policy option. In the long run, they can have detrimental impacts on productivity and market efficiency in a way that negatively impacts workers and consumers. The implementation of price controls should be understood as such and used in periods of sudden and extreme oncoming crises, mitigating sudden cost increases until supply conditions stabilize.

Given the potential long-run risks of price administration with deviations between supply and demand, policy proposals that can directly intervene to mitigate supply shocks should be considered, in addition to traditional price controls. Durable proposals include buffer stocks of strategically important food resources—which already exist to varying degrees for some important commodities such as oil—minimum inventory requirements in supply chains, and central bank style open market operations for key industries. There does not currently exist a comprehensive policy framework to address supply shocks concurrent with price administration programs but warrant future research.

iii. Strengthening Organized Labour

Understanding competition as a contest over profitability between and within industries, the central consideration for firms is how to impact their cost structure. As a result, attempts to reduce costs can often drive down real wages. However, it is organized labour that has pushed back against the worst of these cuts, and at times has succeeded in its struggle to make real wage gains, as was the case in the grocery industry prior to the COVID-19 pandemic.

The main bargaining mechanism of labour is the ability to impose costs on firms that exceed the costs that could be generated through wage increases.17 This is primarily done by withholding productivity through strike actions, or the threat of strikes. Imposing costs on firms creates an imperative for firms to increase wages, as the cost of losing business during a strike has a more significant impact on their profitability than accepting higher wages.

Even more valuable in an inflationary environment following the initial impulse stage, where there is a reduction in the labour share of income as profits balloon during the amplification and propagation stage, unions can restore lost real wages if organized labour is in a position to bargain successfully. Because labour constitutes a smaller cost for firms in this inflationary environment, there is more flexibility for wage increases to restore lost real wages and make new gains.

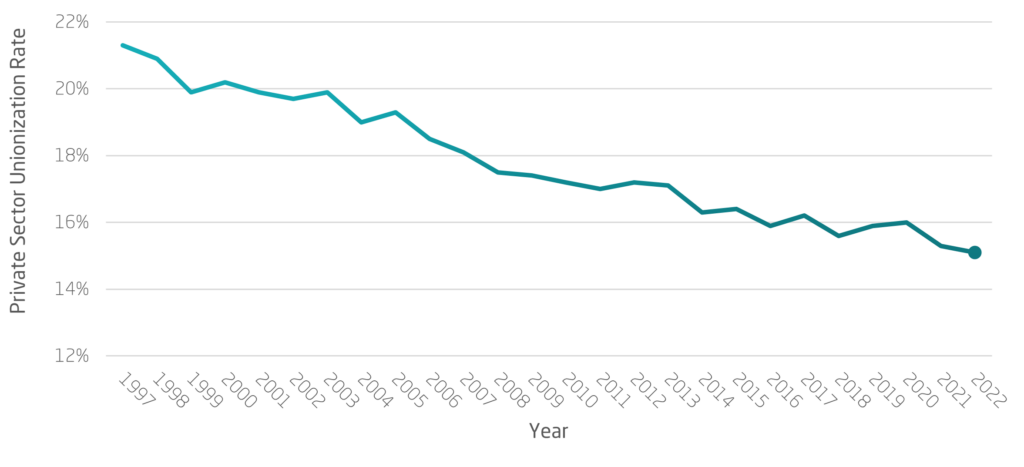

There are two pathways to strengthening organized labour in Canada. First, increasing union density to reinforce the collective power of organized labour as a political and economic force is a primary task that many unions already undertake. Private sector unionization has been on a long decline in recent decades (see Chart 6 for the unionization rate for the wholesale and retail sector in Canada; see Chart 7 for the whole private sector union coverage rate in Canada).

Chart 7 – Private Sector Union Coverage Rate in Canada, 1997-2022

However, strikes held throughout 2023 by workers reacting to their declining real wages and standard of living were mobilized in an organized manner, demonstrating a break from the gradual weakening of labour over several decades. Worker involvement and strong union leadership has won gains across the country, most impressively in the grocery industry where UNIFOR Local 414 won a $4.50/hour wage increase from Metro Inc. over their contract duration in the summer of 2023. Expanding unionization into more sectors can allow for greater incomes for workers as a whole, while also increasing the ability to bargain due to the depression of the general rate of profit from organized labour’s increased bargaining power.

Second, as we see from the competitive dynamics that have played out through the recent episode of grocery industry’s seller’s inflation, bargaining power can be amplified through regulatory changes that limit profitability. However, such gains will not be won in the absence of a political force pushing for them. Beyond bargaining, workers need to collectively push for broader complementary policies that help to reinforce their collective power. This would allow for the aforementioned measures such as windfall taxes and price controls to amplify their position to restore real wages.

Conclusion

Given the existence of price increases in the supply chain alongside passed through prices, a real wage decline, and an increase in profits, seller’s inflation can explain recent developments in the Canadian grocery industry. In addressing this problem and insulating the market against future seller’s inflation, acknowledging the centrality of profits to competitive dynamics, corrective policy recommendations to address affordability and wages in this particular inflationary environment focus on intervening in the market in a way that would modify competitive conditions to curtail profits, incentivize price reductions, and afford cost structure changes to accommodate wage growth. These recommendations include a windfall profit tax, the strengthening and expansion of labour unions, and the development of strategic price controls in systemically significant industries. Together, these three recommendations present limits to the competitiveness of price increases and real wage reductions, and thereby allow for labour to increase its position and support consumers’ ability to purchase food items.

Beyond these immediate proposals intended to generate long-run changes in corporate competition dynamics, it is also useful to consider viable alternatives to the existing grocery retail market. Future research for the long-run sustainability of a grocery industry that exists to deliver necessary services to consumers, food sovereignty, climate crisis mitigation and provide fair-wage jobs to labour should consider nationalized competition dynamics, strategic food stocks, and government administration of food security services.

References

Bernstein, Henry. Class dynamics of agrarian change. Vol. 1. Kumarian Press, 2010

Botwinick, Howard. “Persistent inequalities: wage disparity under capitalist competition.” In Persistent Inequalities. Brill, 2017.

Clifton, James A. “Competition and the evolution of the capitalist mode of production.” Cambridge Journal of Economics 1, no. 2 (1977): 143-151.

Cushen, Jean, and Paul Thompson. “Financialization and value: why labour and the labour process still matter.” Work, employment and society 30, no. 2 (2016): 352-365.

Esping-Andersen, Gosta. The three worlds of welfare capitalism. Princeton University Press, 1990.

Maldonado-Filho, Eduardo. “Competition and equalization of inter-industry profit rates: the evidence for the Brazilian economy, 1973-85.” International Working Group on Value Theory miniconference at the Eastern Economic Association (1998).

Shaikh, Anwar. Capitalism: Competition, conflict, crises. Oxford University Press, 2016.

Shamsuddin, Shomon, and Colin Campbell. “Housing cost burden, material hardship, and well-being.” Housing Policy Debate 32, no. 3 (2022): 413-432.

Skerrett, Kevin, Johanna Weststar, Simon Archer, and Chris Roberts, eds. The contradictions of pension fund capitalism. Labor and Employment Research Association, 2017.

Weber, Isabella M., and Evan Wasner. “Sellers’ inflation, profits and conflict: why can large firms hike prices in an emergency?.” Review of Keynesian Economics 11, no. 2 (2023): 183-213.

Endnotes

- Isabella Weber, et al., “Seller’s Inflation,” 8-11. ↩︎

- Bernstein, Henry, “Class Dynamics,” 101-113. ↩︎

- Capehart, Tom, et al., “Food price inflation,” 3. ↩︎

- Similarly, an industry report by Deloitte indicated that the American average net profit margin in 2023 was at 2.6%, an aberrantly high figure occurring in an inflationary environment similar to the Canadian case. ↩︎

- Shomon Shamsuddin, “Housing cost Burden,” 413-432. ↩︎

- Howard Botwinick, “Persistent inequalities,” 137-172. ↩︎

- Ibid, 25. ↩︎

- Anwar Shaikh, “Capitalism: Competition,” 233-251. ↩︎

- James Clifton. “Competition,” 143-151. ↩︎

- Maldonado-Filho, Eduardo. “Competition and equalization of inter-industry profit rates,” 16-20. ↩︎

- Shaikh, “Capitalism: Competition,” 301-313. ↩︎

- Unfortunately, there is no disaggregated data for working hours by industry. It is aggregated into sectors preventing accurate data. As such, the sector wide trend is identifiable but not anything specific to the grocery industry. ↩︎

- Jean Cushen, “Financialization and Value,” 358-360. ↩︎

- Unfortunately, there is no disaggregated data available for unionization rate for the grocery retail industry-only. It is aggregated into sectors preventing accurate data. As such, the sector wide trend is identifiable but not anything specific to the grocery industry. ↩︎

- For a detailed analysis of the potentials and limits of Canadian pension fund activism, see Skerrit et al. ↩︎

- Esping-Andersen, “Three Worlds,” 26-29. ↩︎

- Botwinick, “Persistent Inequalities,” 198-206. ↩︎

‘Canadian Grocery Profitability: Inflation, Wages and Financialization’ is licensed under CC BY-NC 4.0![]()

![]()

![]()

This project was assisted by the Government of

Canada through the Canada Summer Jobs

Program.